UK E-Invoicing Mandate 2029: Peppol Requirements, Timeline and How to Prepare

UK businesses have time before the UK e-invoicing mandate 2029 takes effect, but waiting for the final technical specification could create operational problems. ERP data, customer records, invoice formats and receiving workflows may all need changes before invoices can move through Peppol. Businesses that delay preparation risk rejected invoices, disrupted accounts-payable processes and slower cash collection when structured e-invoicing becomes mandatory.

The government has confirmed that VAT invoices must be issued and received electronically from 2029 and that Peppol will form the core interoperability network. However, several implementation details remain under development.

What has the UK government confirmed for the 2029 mandate?

The UK government has confirmed mandatory e-invoicing for VAT invoices from 2029. VAT invoices are primarily used for business-to-business and business-to-government transactions where VAT applies.

The Tax Update 2026 also identifies Peppol as the core network for exchanging those invoices. This gives finance teams, software providers and ERP owners a clearer direction for their preparation, even though the final technical rules have not yet been published.

A structured e-invoice is different from a PDF attached to an email. It contains invoice data in a machine-readable format that can be transferred directly between the supplier’s system and the buyer’s system.

This distinction matters because businesses will need more than a process for creating digital documents. They will need systems capable of generating, validating, sending, receiving and processing structured invoice data.

What are the expected Peppol requirements for UK businesses?

Peppol provides a standardised network through which businesses and public authorities can exchange electronic business documents. Companies generally connect through a certified Peppol Access Point rather than creating separate technical connections with every customer or supplier.

Under the expected UK model, businesses are likely to need:

A Peppol-compatible connection or service provider

Structured, machine-readable invoice data

Accurate sender and receiver identifiers

Validation against the applicable invoice rules

A process for handling rejected or incomplete invoices

Integration with the systems used to create and approve invoices

The government has not yet finalised whether the UK will use Peppol PINT directly or introduce a UK-specific profile. A possible PINT UK specification has been discussed, but it should not be treated as a confirmed technical requirement until formal documentation is released.

Businesses should therefore avoid building rigid invoice mappings around assumptions. A configurable integration layer can make it easier to adapt once the final UK format and validation requirements are available.

For more background on the network and document exchange model, read HubBroker’s Peppol e-invoicing guide.

What is the likely UK e-invoicing mandate 2029 timeline?

The confirmed deadline is 2029, but implementation will require preparation well before that date.

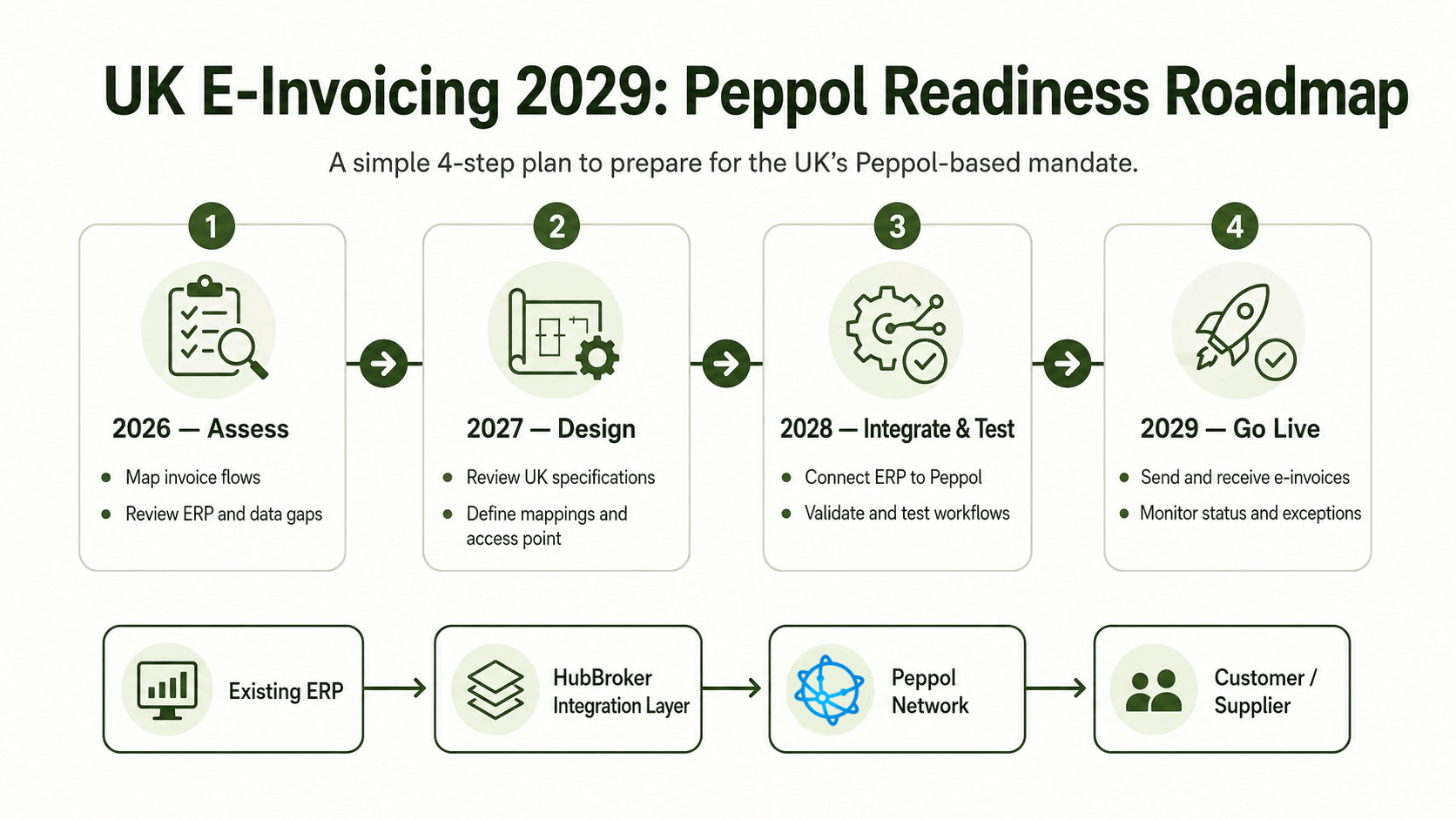

A practical planning timeline is:

2026: Policy development, market engagement and early planning by businesses and software providers.

2027: More detailed technical guidance and specifications may become available.

2028: ERP configuration, invoice mapping, supplier onboarding, testing and exception-process preparation.

2029: Mandatory electronic issuance and receipt of VAT invoices begins.

Only the 2029 mandate has been formally confirmed. The other dates should be treated as planning assumptions rather than statutory milestones.

The lead time is important because e-invoicing projects affect more than invoice transmission. Businesses may need to review tax data, supplier records, customer identifiers, credit-note processes, approval workflows and invoice archiving.

What does the UK e-invoicing mandate 2029 mean for your ERP?

Most businesses already have an ERP or accounting system that creates and records invoices. The objective should not be to replace that system simply to meet the mandate.

Instead, the existing ERP needs to connect with Peppol and the eventual UK invoice specification.

An integration layer can extract invoice information from the ERP, transform it into the required structured format, validate the data and transmit it through a certified Peppol Access Point.

Incoming invoices must also move in the opposite direction. The Peppol invoice should be validated, transformed into a format the receiving ERP understands and delivered to the correct finance workflow.

The integration should also return useful status information. Finance teams need to know when an invoice has been delivered, rejected or blocked because mandatory information is missing.

HubBroker connects Peppol with existing ERP, accounting, EDI and document-processing environments. Its ERP EDI integration services are designed to connect the systems businesses already operate rather than force a rip-and-replace project.

What should finance and IT teams prepare now?

Businesses do not need to wait for every technical detail before beginning readiness work. Finance and IT teams can start by documenting how invoices currently move through the organisation.

The first step is to map all relevant UK VAT invoice flows. Identify which systems create invoices, which channels are used to deliver them and how incoming invoices enter accounts payable.

Teams should then review:

Customer and supplier VAT information

Legal names and addresses

ERP invoice fields

Credit-note and correction workflows

Purchase-order and buyer-reference data

Current invoice formats

Approval and exception processes

Invoice storage and audit requirements

Receiving capability deserves particular attention. A business may prepare to send structured invoices but overlook whether its ERP can import and process invoices received through Peppol.

Supplier and customer onboarding should also be considered. Not every trading partner will be ready at the same time, so businesses may need to support Peppol, EDI, API and legacy invoice channels during the transition.

When should your Peppol implementation begin?

A full UK-specific implementation may be premature until the final format and validation rules are available. However, discovery, data review and integration planning should begin earlier.

Businesses should assess their ERP environment now, identify missing invoice data and choose an architecture that can accommodate changing requirements. A pilot can then be launched once the UK specification is stable enough for meaningful testing.

This approach reduces the risk of discovering late in the project that invoice data is incomplete, receiving workflows are manual or ERP changes require more development than expected.

Review your UK invoice flows with HubBroker to identify the ERP, data and Peppol changes that should be addressed before formal testing begins.