60 Days to the French Mandate: A Readiness Checklist for Finance Teams

The French e-invoicing reform is no longer a distant compliance project. Finance teams now have a limited window to confirm their systems, invoice data, workflows and service providers are ready.

This French e-invoicing checklist provides a practical 60-day plan for finance, accounts payable, accounts receivable and IT teams. The aim is not simply to meet the deadline, but to prevent rejected invoices, manual work and payment delays after the mandate begins.

What changes on 1 September 2026?

From 1 September 2026, every business subject to French VAT must be able to receive electronic invoices, regardless of its size. Large companies and mid-sized companies must also issue electronic invoices and complete the required e-reporting from that date.

Small businesses, microbusinesses and most SMEs have until 1 September 2027 to begin issuing electronic invoices, but their receiving systems must still be ready in 2026. rd PDF attached to an email will not meet the new definition of an electronic invoice. Invoices must contain structured data, follow an accepted format and be exchanged through a French Plateforme Agréée, or PA. ur business affected by the French e-invoicing mandate?

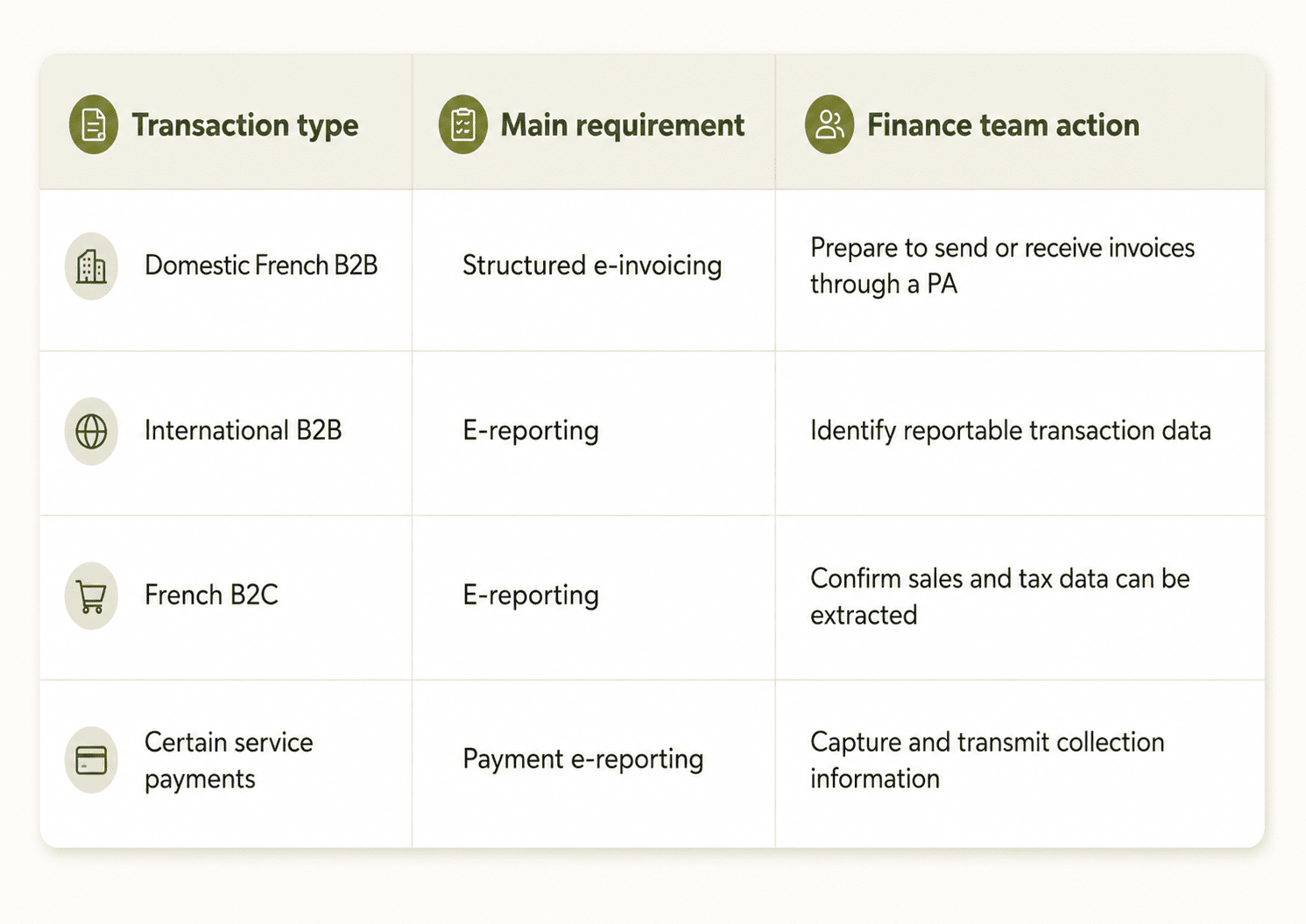

The reform covers domestic B2B transactions between businesses established in France and subject to French VAT. It also introduces e-reporting requirements for certain B2C and international transactions, as well as payment reporting for relevant services. teams should separate their transactions into three categories:

This classification should be completed before technical configuration begins. Otherwise, teams may build invoice workflows without covering all reporting obligations.

What should be included in a French e-invoicing checklist?

A useful readiness checklist must cover more than invoice format. It should confirm that your invoice data, ERP, customer records, supplier records, tax rules and approval processes can support the complete invoice lifecycle.

Check the following areas:

Confirm which French entities and VAT registrations are in scope.

Document current inbound and outbound invoice processes.

Select your PA or confirm how your existing provider connects to one.

Review customer and supplier identification data.

Confirm your ERP can produce the required structured invoice information.

Map invoice statuses, credit notes and payment information.

Define how rejected invoices and missing data will be handled.

Test realistic invoice scenarios before production.

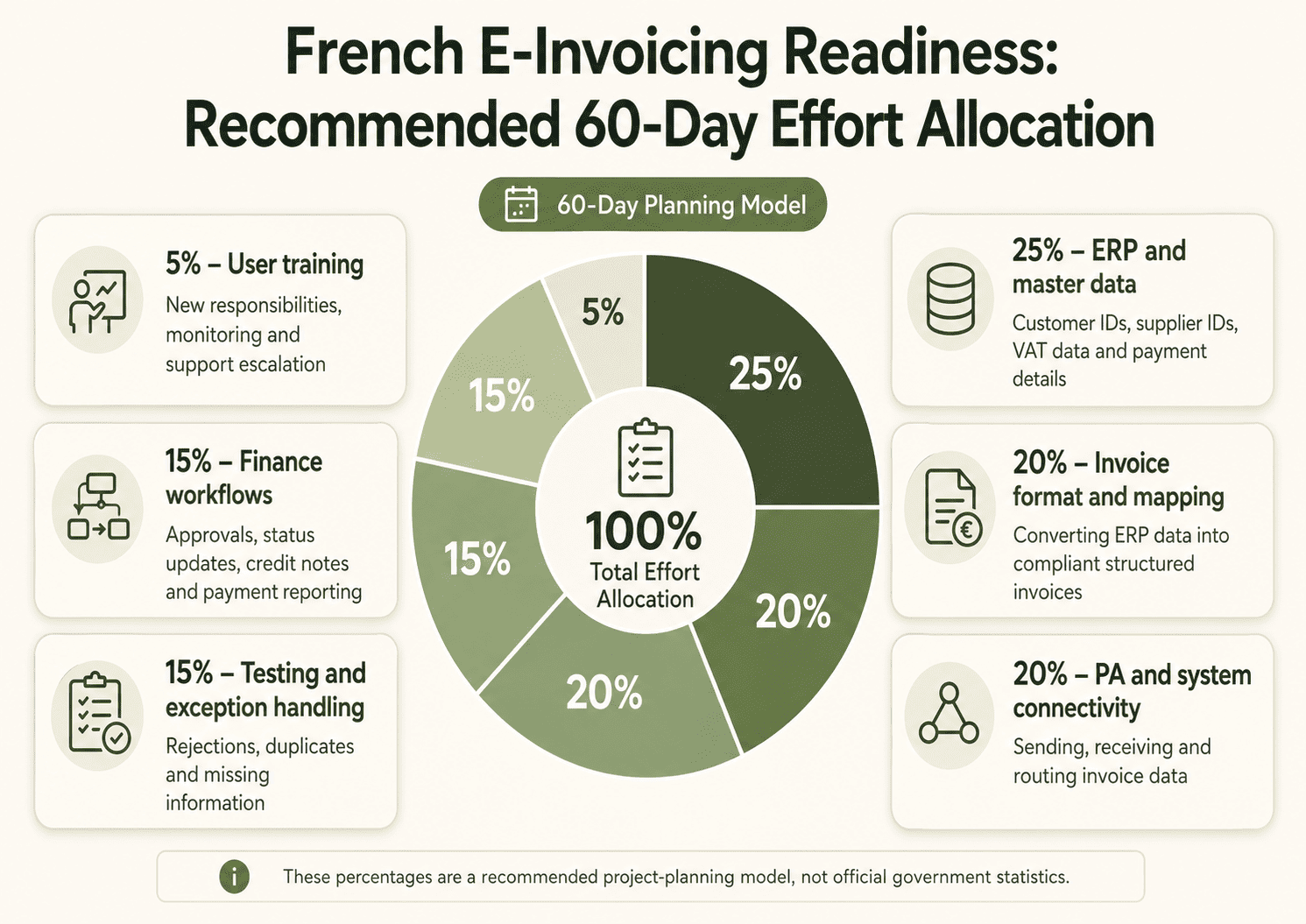

How should finance teams use the final 60 days?

Do not leave all configuration and testing until the final weeks. Divide the remaining work into controlled phases.

Finance should own the business requirements, while IT or the integration provider manages connectivity and data transformation. Both teams should jointly approve the final test results.

Finance should own the business requirements, while IT or the integration provider manages connectivity and data transformation. Both teams should jointly approve the final test results.

Which invoice formats and data fields should be tested?

France accepts structured formats including UBL, CII and mixed formats that combine structured invoice data with a readable document. Required information must appear in dedicated data fields rather than only in a visual PDF. ting should include:

Supplier and customer identifiers

Invoice number and issue date

VAT numbers, rates and amounts

Delivery address where required

Payment terms and due dates

Purchase order references

Credit notes and invoice corrections

Invoice lifecycle statuses

Duplicate and rejected invoice scenarios

Do not test only one perfect invoice. Use missing references, incorrect tax values, duplicate documents and incomplete customer records to confirm how the system handles real exceptions.

These percentages are a recommended project-planning model, not official government statistics.

What should your e-invoicing test plan include?

A successful test should follow the invoice from the ERP to the receiving platform and back into the finance workflow. Confirm that the recipient can be identified, the document passes validation, the status is returned and the final invoice is available in the correct finance system.

Test at least one scenario for every major customer type, invoice type, VAT treatment and business entity. Large-volume businesses should also test batch processing and peak invoice periods.

A practical way to prepare with HubBroker

The final weeks before the mandate should be spent resolving issues, not designing the integration from the beginning. HubBroker helps finance and IT teams connect their existing systems with structured e-invoicing and document-exchange workflows. Its platform supports ERP integration, mapping, validation, monitoring and automated document processing. es choose HubBroker because they can:

Connect existing ERP and finance systems instead of replacing them.

Map current invoice data into required structured formats.

Validate invoice fields before documents are transmitted.

Automate inbound and outbound invoice workflows.

Monitor invoice delivery, processing and rejection statuses.

Support wider European e-invoicing and Peppol requirements.

Work with an integration team through setup, testing and go-live.

The French mandate is a compliance deadline, but it is also an opportunity to remove manual invoice handling. Start with a readiness review, identify the remaining gaps and test the complete process before 1 September 2026.

Prepare your French e-invoicing workflow with HubBroker. Book a consultation to review your ERP, invoice formats, transaction volumes and integration requirements.