ViDA Update What Changed in the Latest EU Council Vote

Quick Questions About ViDA

What is ViDA in the EU?

ViDA, or VAT in the Digital Age, is the European Union’s reform package to modernize VAT rules for digital business, e-invoicing, real-time VAT reporting, platform economy transactions, and cross-border VAT registration. The latest EU Council agreement confirms that VAT reporting for cross-border transactions will become fully digital by 2030.

What changed in the latest EU Council vote on ViDA?

The latest Council agreement confirmed three major changes: cross-border VAT reporting will become digital through e-invoicing, online platforms may become responsible for VAT on short-term accommodation and passenger transport services, and the EU’s VAT one-stop-shop system will be expanded to reduce the need for multiple VAT registrations.

When will ViDA e-invoicing become mandatory?

Under the Council agreement, the EU digital VAT reporting system should be in place by 2030. Businesses will issue structured e-invoices for cross-border B2B transactions and automatically report invoice data to their tax administration. Existing national systems are expected to become interoperable with the EU system by 2035.

Does ViDA mean PDF invoices will no longer be enough?

For cross-border B2B VAT reporting, ViDA moves businesses toward structured e-invoices instead of manual or PDF-based invoice processes. This means companies should prepare their ERP, accounting, EDI, and e-invoicing systems to generate invoice data in a structured format that can support automated VAT reporting.

How should businesses prepare for ViDA?

Businesses should start by reviewing their EU invoice flows, VAT codes, ERP integrations, customer and supplier data, and e-invoicing readiness. Companies operating across multiple EU countries should also check whether they need Peppol, EDI, or country-specific e-invoicing connectivity to stay compliant as national and EU-wide rules develop.

Introduction

The EU’s VAT in the Digital Age, commonly known as ViDA, is no longer just a long-term tax reform discussion. The latest EU Council decision has moved the package closer to practical implementation, especially for companies dealing with cross-border invoicing, VAT reporting, platform sales, and multi-country VAT registration.

The Council reached agreement on a package designed to modernize VAT rules through electronic invoicing, real-time digital reporting, platform economy VAT rules, and expanded VAT one-stop-shop mechanisms. According to the Council, the aim is to fight VAT fraud, support businesses, and promote digitalisation across the EU.

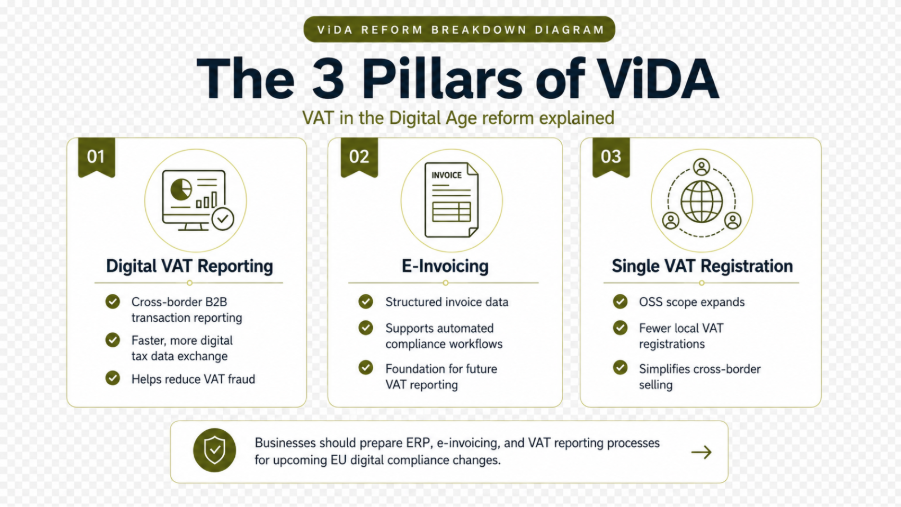

What Is ViDA?

ViDA stands for VAT in the Digital Age. It is the EU’s reform package to update VAT rules for a more digital economy. The reform focuses on three major areas:

Digital VAT reporting and e-invoicing

VAT treatment of platform economy operators

Single VAT registration through expanded one-stop-shop systems

The Council agreement covers three legal acts: a directive, a regulation, and an implementing regulation. Together, these update different parts of the EU VAT framework.

The Biggest Change: Cross-Border VAT Reporting Goes Digital

The most important update for B2B companies is the shift toward fully digital VAT reporting for cross-border transactions by 2030. Today, many businesses submit periodic recapitulative statements to national tax authorities. These reports are not real-time, and the Council notes that this delay creates room for fraud because authorities do not receive complete transaction data quickly enough.

Under ViDA, businesses involved in intra-EU B2B transactions will issue structured e-invoices and automatically report the relevant invoice data to their tax administration. This reporting will be based on the existing European e-invoicing standard used in public procurement. National tax administrations will then share the data through a new EU-level IT system.

For finance teams, this means invoice creation, validation, tax reporting, and audit readiness will become much more connected. PDF invoices and manual reporting processes will become less practical for EU cross-border trade.

E-Invoicing Becomes the Foundation of Compliance

ViDA does not treat e-invoicing as a separate IT upgrade. It makes e-invoicing the foundation for future VAT reporting.

This is a major shift. Businesses will need invoice data that is structured, validated, and ready for automated reporting. That means finance and IT teams should start reviewing how their ERP, accounting, EDI, and e-invoicing systems currently handle invoice formats, tax fields, buyer/supplier identifiers, credit notes, and cross-border VAT treatment.

The Council also agreed that the EU system should be in place by 2030, while existing national digital reporting systems should become interoperable with the EU system by 2035.

Prepare for ViDA E-Invoicing Updates in 2026

Get your business ready for EU VAT and e-invoicing changes with HubBroker’s compliant e-invoicing, Peppol, and ERP integration solutions.

Contact Us to Know More

What Changed for Digital Platforms?

ViDA also changes how VAT applies to parts of the platform economy. Under the agreed rules, online platforms may become responsible for collecting and remitting VAT for certain services, especially short-term accommodation rentals and passenger transport, where the underlying service provider does not charge VAT. This is known as the deemed supplier model.

The latest Council position also added more flexibility for member states. It expanded the definition of short-term accommodation rental for tax purposes and allows member states to exempt some SMEs from the deemed supplier rules.

For platform operators, this means VAT compliance may no longer sit only with the individual seller, host, or driver. Platforms will need stronger controls for VAT status checks, transaction classification, tax calculation, invoice data, and reporting.

One-Stop-Shop Rules Are Expanding

Another important change is the expansion of VAT one-stop-shop mechanisms. Currently, one-stop-shop systems allow businesses to declare and pay VAT for certain cross-border B2C sales through one member state. However, businesses can still face extra VAT registrations when selling goods inside another member state, such as from a local warehouse.

The Council agreement extends the scope of one-stop shops to more B2C supplies, including certain domestic supplies such as electricity and gas. It also covers situations where companies move stock into another member state to sell directly to consumers later.

This should reduce the need for multiple VAT registrations, but it will also increase the importance of clean transaction data and correct country-level VAT treatment.

Mandatory Reverse Charge for Some B2B Transactions

The Council also agreed to shift VAT liability from the supplier to the buyer in certain B2B transactions where the supplier is not established in the member state where VAT is due. This is the reverse charge mechanism. While this already exists in some cases, the Council says it will become mandatory in the future.

For businesses, this means tax logic inside ERP and invoicing workflows must be reviewed carefully. Incorrect reverse charge handling can lead to invoice rejections, tax reporting errors, and reconciliation issues.

What Did the Council Decide Not to Include?

The latest Council position also narrowed some parts of the original proposal. The Council decided not to extend the existing deemed supplier provision to all goods supplied by online platforms and transfers of own goods. It also agreed not to change rules on works of art and antiques.

This matters because it shows ViDA is not a single blanket rule for every transaction type. Businesses will need to assess their exact transaction flows, countries, customer types, and supply models.

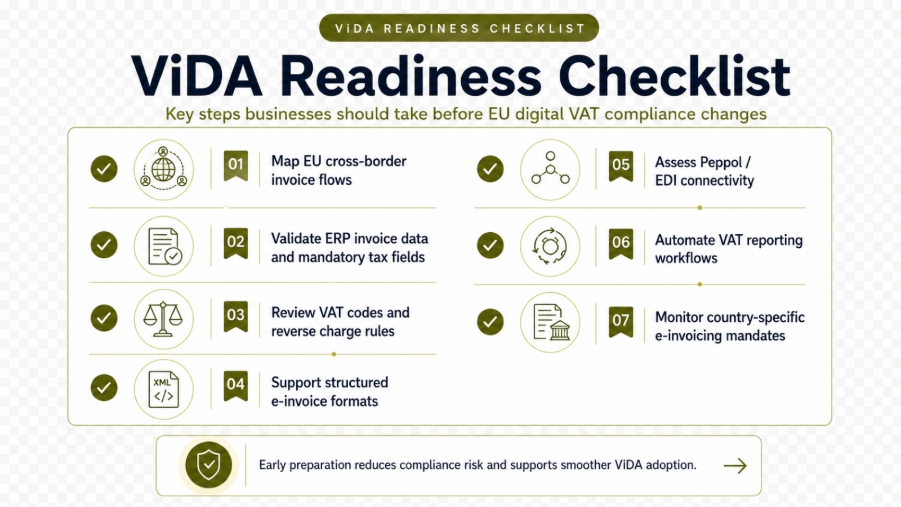

What Businesses Should Do Now

ViDA may feel like a 2030 deadline, but waiting is risky. Several EU countries are already moving ahead with national e-invoicing and digital reporting mandates. Businesses should start by mapping current invoice flows across ERP, EDI, accounting, and tax systems.

Key preparation steps include:

Identify all EU cross-border B2B transaction flows.

Check whether invoices are structured or still PDF-based.

Review VAT fields, buyer IDs, supplier IDs, tax codes, and credit note handling.

Assess ERP readiness for e-invoicing and reporting.

Plan integration with Peppol, EDI, or other national e-invoicing networks.

Prepare for country-by-country mandate differences before full EU harmonisation.

Prepare Your Business for the ViDA E-Invoicing Changes

The EU’s ViDA initiative is reshaping how businesses manage VAT reporting and cross-border e-invoicing. As new requirements move closer, companies need reliable systems that can handle structured invoice data, compliance updates, and seamless digital exchange.

HubBroker helps businesses prepare for ViDA with scalable e-invoicing, Peppol, EDI, and ERP integration solutions designed for European compliance.

Get in touch with HubBroker to make your e-invoicing process ViDA-ready.