E-Invoicing Compliance Checklist for CFOs

Introduction

E-invoicing mandates are shifting from future planning to operational deadlines. For CFOs, the risk is no longer limited to invoice automation it now affects compliance exposure, VAT reporting, supplier payments, and finance continuity.

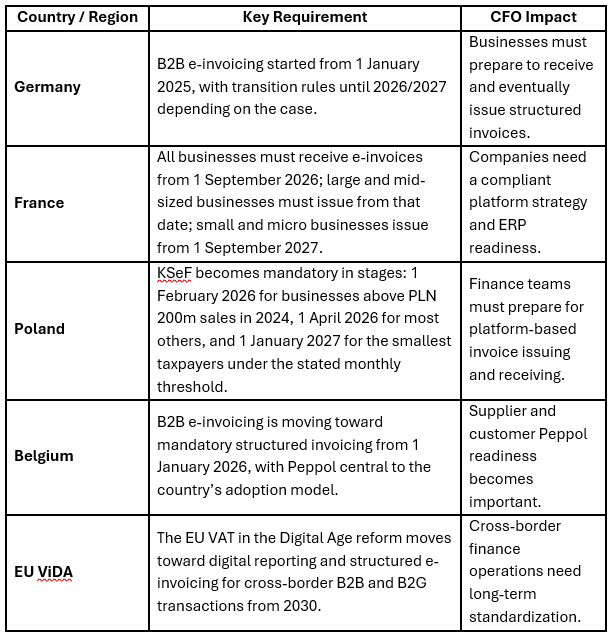

Across Europe and beyond, governments are moving away from paper and PDF invoices toward structured, machine-readable invoice data. France, Germany, Poland, Belgium, the UAE, and other countries are introducing or expanding e-invoicing and real-time reporting requirements. In France, for example, all businesses must be able to receive electronic invoices from 1 September 2026, while large and mid-sized companies must also issue them from that date. Smaller businesses follow for issuing from 1 September 2027.

For CFOs, the question is no longer: “Do we need e-invoicing?”

The better question is: “Are our finance systems ready before the mandate reaches us?”

Why CFOs Can No Longer Treat E-Invoicing as an IT Project

E-invoicing affects IT systems, but the business risk belongs to finance.

A failed e-invoicing setup can delay supplier payments, interrupt invoice approvals, create VAT reporting errors, and increase compliance exposure. That makes it a CFO-level priority, not just a software configuration task.

The reason is simple: e-invoicing changes how invoice data is created, validated, transmitted, received, archived, and reported. In Germany, for example, since 1 January 2025, a valid e-invoice must be issued, transmitted, and received in a structured electronic format that allows electronic processing. A simple PDF is no longer treated as an e-invoice under the new definition.

For CFOs, this means invoice compliance now depends on:

The quality of master data

ERP readiness

Supplier and customer onboarding

Tax reporting accuracy

Digital archiving

Approval workflow automation

Integration between finance systems and external networks

What E-Invoicing Changes Inside Your Finance Operations

E-invoicing changes the finance process from document handling to data handling.

In a traditional invoice process, finance teams often deal with PDFs, email inboxes, manual entry, spreadsheet checks, and delayed approvals. Under structured e-invoicing, invoice data must be captured, validated, exchanged, and stored in a compliant digital format.

That affects both accounts payable and accounts receivable.

For AP teams, incoming invoices may need to be received through a Peppol Access Point, national platform, or approved service provider. For AR teams, invoices must be generated in the right format before they are sent to customers or reported to tax authorities.

The biggest operational changes include:

Invoice creation

Invoices must contain structured data, not just human-readable text.

Validation

Invoice fields must match country-specific rules, tax IDs, VAT logic, buyer references, and format requirements

Transmission

Invoices may need to move through approved networks such as Peppol, KSeF, PDP/PA, or other national platforms.

Reception

Businesses must be able to receive and process structured e-invoices, not only send them.

Archiving

The structured invoice data must be stored correctly for audit and tax purposes.

Stay Ahead with an E-Invoicing Compliance Checklist for CFOs

Ensure your finance team is prepared for changing e-invoicing rules, structured invoice formats, and country-specific compliance requirements.

Contact Us to Know More

Global E-Invoicing Deadlines: What CFOs Should Prepare For

The e-invoicing timeline is not global in one single step. It is country-by-country, format-by-format, and mandate-by-mandate.

Here are key examples CFOs should track:

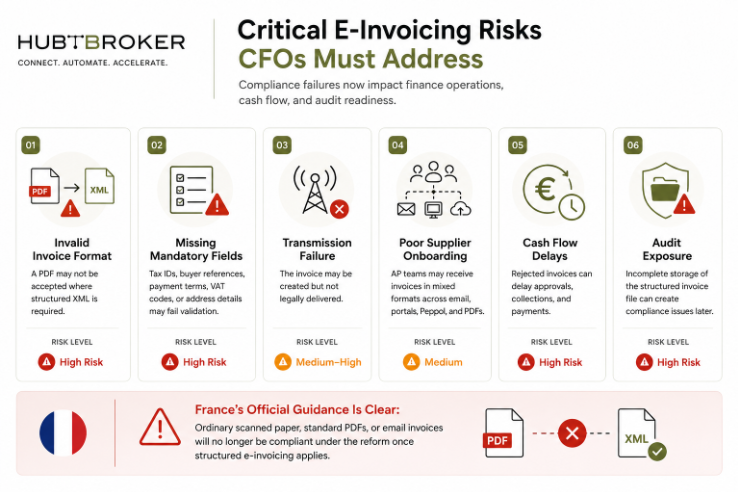

The Compliance Risks and Requirements You Need to Know Now

The biggest e-invoicing risk is assuming that your ERP already handles everything.

Most ERP systems can create invoice data, but compliance often requires more: format validation, country-specific fields, transmission through a certified or approved network, response handling, invoice status tracking, and audit-ready storage.

E-Invoicing Readiness Checklist for CFOs and Finance Teams

Use this checklist before choosing or expanding your e-invoicing solution.

Finance process readiness

Have you mapped your current AP and AR invoice flows?

Do you know which countries, entities, and VAT registrations are affected?

Are invoice approval workflows documented?

Do you know where invoice rejections usually happen today?

ERP and integration readiness

Can your ERP generate structured invoice data?

Can it receive structured invoice files?

Are invoice fields mapped correctly to local formats?

Do you need middleware, API integration, or an iPaaS layer?

Compliance readiness

Which formats apply: Peppol BIS Billing 3.0, XRechnung, Factur-X, UBL, CII, KSeF, or another local format?

Do invoices pass validation before they are sent?

Is the correct tax and business data included?

Is the structured file archived, not just the PDF view?

Network and platform readiness

Do you need a Peppol Access Point?

Do you need a PDP/PA connection in France?

Do you need KSeF integration in Poland?

Do you have a fallback process for exceptions?

Supplier and customer readiness

Which customers already require e-invoices?

Which suppliers can send structured invoices?

Do you have a rollout plan for trading partners?

Can your team support mixed formats during transition?

Practical Steps to Get Started with E-Invoicing Compliance

CFOs do not need to solve every country mandate on day one. The practical approach is to build a reusable compliance foundation.

Start with these steps:

Identify affected countries and entities

List where your company sells, buys, pays VAT, or receives supplier invoices.

Audit your invoice formats

Check how many invoices are PDF, XML, EDI, Peppol, portal-based, or manually entered.

Review ERP capabilities

Confirm what your ERP can generate, receive, validate, and archive.

Choose the right integration layer

An iPaaS or middleware layer can connect your ERP, Peppol Access Point, IDP solution, and national platforms.

Automate invoice capture for non-standard inputs

Use IDP where suppliers still send PDFs or semi-structured documents.

Test before the deadline

Run pilot flows with selected suppliers and customers before mandates become mandatory.

Build a monitoring dashboard

Track sent, received, rejected, pending, approved, and archived invoices.

This is where HubBroker can support finance teams with EDI, Peppol Access Point connectivity, ERP integration, IDP, and PDF to XML conversion in one connected workflow.

E-Invoicing Compliance FAQ for CFO

Is e-invoicing only about replacing PDF invoices?

No. E-invoicing is about structured, machine-readable invoice data. A PDF may still be useful for human viewing, but many mandates require structured formats that systems can validate and process automatically.

Does our ERP already make us compliant?

Not always. Your ERP may generate invoice data, but compliance may still require format conversion, network transmission, validation, archiving, Peppol connectivity, or country-specific reporting.

What is the role of Peppol?

Peppol is a secure network used to exchange electronic business documents, including invoices, between registered participants. It is widely used in Europe and also adopted in markets outside Europe.

What should CFOs prioritize first?

Start with country exposure, invoice volume, ERP capability, supplier readiness, and upcoming deadlines. Then build a phased roadmap instead of reacting country by country.

Conclusion: E-Invoicing Is a Finance Transformation Opportunity

E-invoicing compliance should not be treated as a last-minute tax project. For CFOs, it is a chance to reduce manual work, improve invoice accuracy, accelerate approvals, strengthen VAT compliance, and gain better visibility across finance operations

The companies that prepare early will not just meet mandates. They will build cleaner, faster, and more scalable finance processes.

Need help preparing your finance systems for e-invoicing mandates?

HubBroker helps businesses connect ERP systems, automate invoice processing, convert PDFs, and exchange compliant e-invoices via Peppol and EDI.